Helping Seniors with Daily Financial Management

As Americans enter old age in rapidly increasing numbers, more money management consultants will run into situations like the one a Virginia CPA encountered last year. The CPA spent five hours rummaging through the home of a 94-year-old client, trying to find the paperwork needed to complete the man’s 2010 tax return.

The client, a high-net-worth individual who always had kept his financial affairs in order, had become disorganized and disoriented, with papers strewn throughout his house and uncompleted tasks piling up. Seeing that his client needed ongoing help that he could not provide, the Virginia CPA turned to a former colleague who specializes in providing such assistance.

Barbara Green, CPA, had begun a career as a daily money manager in fall 2010 after 25 years in public practice and 5½ years with the U.S. Department of Defense’s Office of Inspector General. Now one of the great financial money management consultants, she does work for people who can’t or won’t do such tasks themselves. In the case of the 94-year-old man, he had a complicated financial situation that he could no longer handle on his own.

“He was throwing things away that needed to be kept,” Green said.

So Green worked with the man’s grandson to organize his affairs. On an ongoing basis, she reconciles accounts, ensures that bills are paid and even sorts through the mail. She also consults with the 94-year-old to answer financial questions for senior citizens and help him complete essential tasks.

A PROBLEM GROWING WITH AGE

Demand for the money management for seniors services that Green provides is growing largely due to the rapid graying of the U.S. population. Consider the following:

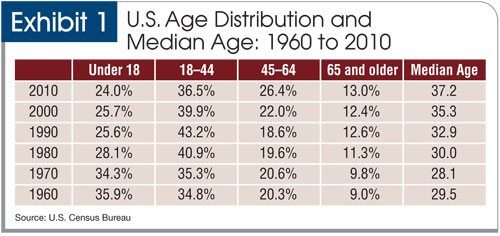

- The number of Americans at least 80 years old jumped by more than 20% between 2000 and 2010, according to the 2010 U.S. Census. The number of 90-year-olds soared by 30%. The U.S. median age rose to 37.2, from 35.3 in 2000 and 28.1 in 1970 (see Exhibit 1).

- The baby boomer generation is beginning to rush past retirement age. The first set of baby boomers turned 65 in 2011. Between 2000 and 2010, the number of people age 60 to 64 soared more than 55%, while those age 55 to 59 leaped 46%—the two largest increases among all U.S. age groups. As of the 2010 Census, there were slightly more than 40 million people age 65 and over. That number is projected to reach 72 million in 2030.

Why are these facts important to CPAs and money management consultants? Because older people are much more likely to develop dementia, Alzheimer’s disease and other ailments that affect their ability to manage finances. In the case of Alzheimer’s disease, which is the most common form of dementia, symptoms in 95% of cases don’t appear until after age 60, and the risk of developing it rises rapidly after age 65, according to the National Institute on Aging, part of the National Institutes of Health.

James Sullivan, CPA/PFS, a Chicago-based expert in how accountants should handle elder-care issues, recommends that money management consultants ready themselves to deal with the complications that come with an aging client base. “Any CPA firm that works with individuals on an ongoing basis will face these issues,” he said.

Sullivan co-authored a JofA article (“CPAs in an Aging Society: When Alzheimer’s Disease Affects a Client,” Jan. 2010, page 44) that outlined ways for CPAs to deal ethically with clients suffering from diminished mental acuity. This article deals with the emerging field of daily money management (DMM) and examines the opportunities and challenges for CPAs in providing or overseeing the services money management consultants handle.

WHAT MONEY MANAGEMENT CONSULTANTS DO

Jackie Bell, CPA, worked in corporate finance for most of the first 27 years of her career. She started doing DMM in 2005 after hearing about the concept in a radio commercial. She now provides DMM and tax services in the Rochester, N.Y., area. Of her 40 clients, a dozen receive DMM assistance. The others receive tax services.

The average age of Bell’s DMM clients is between 80 and 85, she said. The duties she performs are typical for money management consultants. In addition to bill paying, checkbook balancing and going through mail, she does investment and insurance reviews, keeps track of assets and coordinates with other financial professionals.

“Sometimes I can help interpret … when my clients are dealing with someone they don’t understand, like investment advisers,” Bell said.

TAKING CARE OF THE PARENTS

Many CPA firms could boost their bottom lines by adding bill-paying and other services for elderly clients, said Ted Sarenski, CPA/PFS, president and CEO of Syracuse, N.Y.-based Blue Ocean Strategic Capital and the chairman of the AICPA PFP Executive Committee’s Elder Planning Task Force.

Sarenski sees an opportunity for CPA firms to act in a supervisory role overseeing the delivery of services. Not all of those services would have to be financial in nature. For example, CPA firms could contract with a lawn service to get clients’ yards mowed or with a maintenance service to handle home repairs.

In the past, when people got older and began to require assistance with daily tasks, either due to physical ailments or mental problems, their children usually were the ones who provided help.

“They went over and helped mom or dad write the checks for that month,” Sarenski said. “They went over and mowed the lawn for them.”

Such scenes are less common today. Adult children are much more likely to live a considerable distance from their parents than in previous generations, making it virtually impossible for them to provide direct assistance on day-to-day matters.

“(The children) still have that desire to take care of their parents, as the past generation did,” Sarenski said. “And their way of doing it will be … to hire (outside help).”

Pete Conklin, a DMM based in northern Virginia and president of the American Association of Daily Money Managers, said he gets “tons of referrals” from adult children who have moved to other parts of the country and can’t keep making the trips back home to deal with their parents’ issues.

WHERE DO CPA FIRMS FIT IN?

Still, children aren’t the top referral sources for money management consultants. Green reports that her best client tips come from CPA firms and estate attorneys. Bell points to geriatric care managers and attorneys as her top referral sources, while Conklin, who has between 13 and 15 DMM clients, puts social workers and program managers in retirement communities at the top of his list, followed by CPAs and estate attorneys.

Why would a CPA firm refer a client to money management consultants rather than provide the needed services? One reason is that rates for DMM work pale in comparison to typical CPA fees. Green’s and Bell’s fees for organizing and bill-paying services range from $75 to $90 an hour—well below the three-figure rates they enjoyed in previous jobs. Conklin earns $95 per hour, but he also provides transportation to medical appointments and other services that most money management consultants don’t offer.

Some DMMs in high-priced markets, such as New York, charge rates as high as $150 to $200 an hour, but they are not the norm. Driving down rates is competition from others, such as geriatric care managers, who sometimes provide money management consultants services for as low as $40 an hour.

Still, Bell views her job as potentially lucrative, in part because CPAs in the DMM field can make additional money offering specialized services such as tax preparation and planning and long-term-care planning. Green lets clients know that she can offer more analytical work than basic bill paying but that those services will command higher fees. Bell and Green both benefit because they work out of their homes and don’t have the overhead costs of a CPA firm.

Green sees daily money management as a good option for CPAs looking to do something different at the end of their careers, but she thinks it would be a challenge for many CPA firms to get involved in the practice.

Sarenski argues that some CPA firms could make DMM work viable by hiring less expensive personnel to perform the actual tasks.

“You don’t have to have a CPA to write a check for the utility bill that month for someone,” Sarenski said. “So you may be hiring a clerk-level person to do a lot of the paperwork, with the CPA overseeing everything to make sure that it’s accounted for properly.”

Sarenski suggests that, for high-net-worth clients, CPA firms could grow their service offerings to include tasks such as finding home care, making plane and hotel reservations and helping with the purchase of a car.

“It could involve being their personal concierge, if you will,” he said.

Rates are not the only reason some CPA firms might be reluctant to go into DMM. Sarenski’s firm, Blue Ocean Strategic Capital, does not provide DMM services because it handles investment management for clients. Adding bill-paying services likely would involve Blue Ocean’s gaining access to clients’ money to write checks. Having such access while also making investment decisions for clients would subject the firm to much heavier SEC scrutiny, including surprise audits.

That would not be a problem for CPA firms that don’t provide investment services, Sarenski said.

MAKING A DIFFERENCE

Even if they don’t directly handle services such as bill paying for senior clients, CPAs likely will have to deal with the ramifications of financial decisions made by older clients, DMMs or elder-care providers.

To perform this oversight role effectively, CPAs working with older clients need to understand how geriatric illnesses progress to anticipate the kind of care their clients will need and how much that care will cost, Sullivan said. Only then can the CPA come up with a plan that will make the clients’ assets last for as long as possible while still paying for the needed care.

Another area where CPAs can play a role is in fraud detection. Sullivan tells the story of being called in by a geriatric care manager to look over the finances of an elderly woman with cognitive issues whose accountant had retired and passed her business on to another firm. The geriatric care manager asked Sullivan to review the woman’s bills and, in the course of doing so, he discovered that the new bookkeeper had charged her more than $6,000 over three months for work that Sullivan said should have cost no more than $250.

“When we got involved and started looking at the bills this bookkeeper was charging, it was akin, to me, of elder financial abuse,” Sullivan said. “Another thing accountants can pay special attention to in working with clients, whether they’re old clients or new, is to look for this kind of abuse. Since we got involved, the woman has been put under guardianship, and the attorney involved is going to go and seek restitution of the funds.”

The opportunity to help people motivates money management consultants such as Green, Bell and Conklin, who all provide pro bono work for clients who can’t afford to pay. And while Bell believes her business has moneymaking potential, what’s most important to her is the satisfaction she gains from helping her clients.

“There are some times when I leave an appointment with a fairly new client, and I’ll shake my head because I don’t know what they’d do without me,” Bell said. “And I’m not saying that because I’m good at what I’m doing. I’m saying that because they have no way to do this themselves.”

That’s a message that Green believes all CPAs need to hear.

“I would just like to get the idea out there, because when I go to meetings and I meet other CPAs and tell them what I’m doing now, nobody’s ever heard of it before,” she said. “I just wonder why they don’t know this, because obviously they have clients who go into various stages of dementia or whatever other kinds of problems they have. There have to be other people out there who need this kind of service.”

Other Types of DMM Clients

The elderly are not the only client group for money management consultants. Money management consultants also work with busy professionals who either don’t have the time or the desire to deal with their finances. Some of these clients can be quite young. Pete Conklin, a DMM based in northern Virginia, works with three clients who are in their 20s but choose to pay for outside financial help because of extensive travel and packed schedules.

Other types of DMM clients include those with physical ailments such as poor eyesight, arthritis or Parkinson’s disease. Barbara Green, CPA, another DMM based in northern Virginia, works with a client whose body shakes so much she can barely write. Other DMMs specialize in helping people with attention deficit hyperactivity disorder who have trouble organizing their affairs.

Ted Sarenski, CPA/PFS, head of the AICPA PFP Executive Committee’s Elder Planning Task Force, points out that a handful of CPAs have provided DMM-type services for decades to professional athletes, movie stars and other performers in places such as Hollywood, New York City and Las Vegas. Andrew Blackman, CPA/PFS/CFF, has been working as a business manager for entertainers since 1979. As a partner with CPA firm Shapiro Lobel LLP in New York City, Blackman makes daily cash decisions, pays bills, keeps books and records, and coordinates the work of other professionals on numerous other critical financial services for a host of clients, including several Broadway and film actors. The job pays well. Blackman’s firm usually gets either 5% of his clients’ professional earnings or a flat hourly rate that varies with the staff on an assignment. His personal rate to supervise this work is $450 an hour.

EXECUTIVE SUMMARY

Once people hit age 65, they encounter a risk of dementia and other conditions that rises rapidly with age and can leave them unable to handle even simple financial responsibilities. As the number of Americans 65 and older grows, more people will need help with bill-paying and other money-management tasks.

Once people hit age 65, they encounter a risk of dementia and other conditions that rises rapidly with age and can leave them unable to handle even simple financial responsibilities. As the number of Americans 65 and older grows, more people will need help with bill-paying and other money-management tasks.

Daily money managers provide services such as sorting through mail, paying bills, interfacing with other financial professionals, doing investment and insurance reviews, and keeping track of assets.

Barbara Green, a CPA and DMM, sees DMM as a good option for CPAs looking to do something different toward the end of their careers.

The head of the AICPA PFP Executive Committee’s Elder Planning Task Force argues that certain accounting firms could make money providing bill-paying and other services. The firms could make the business viable by hiring lower-paid staff to perform the actual tasks, which would be overseen by CPAs.

CPAs need to understand geriatric illnesses so they can properly prepare financial plans that cover long-term care for clients.

CPA firms that perform investment services face greater SEC scrutiny, including surprise audits, if they try to handle bill-paying services directly. Another impediment to CPA firms’ taking on DMM themselves is lower billing rates.

Jeff Drew is a JofA senior editor. To comment on this article or to suggest an idea for another article, contact him at jdrew@aicpa.org or 919-402-4056.

AICPA RESOURCES

JofA article

“CPAs in an Aging Society: When Alzheimer’s Disease Affects a Client,” Jan. 2010, page 44

Publication

Management of an Accounting Practice Handbook (#MAP-XX, online subscription; #090407, loose-leaf)

For more information or to make a purchase, go to cpa2biz.com or call the Institute at 888-777-7077.

Website

Elder Planning Task Force home page

PFP Member Section and PFS credential

Membership in the Personal Financial Planning (PFP) Section provides access to specialized resources in the area of personal financial planning, including complimentary access to Forefield Advisor. Visit the PFP Center at aicpa.org/PFP. Members with a specialization in personal financial planning may be interested in applying for the Personal Financial Specialist (PFS) credential. Information about the PFS credential is also available at aicpa.org/PFS.